Fiscal policy, the second factor, may therefore be more important in explaining buoyant prices. In a normal recession, as people lose jobs and their incomes fall, foreclosures drag house prices down—not only by adding to the supply of houses on the market, but also by leaving ex-home-owners with a blemish on their credit history, making it harder for them to borrow again. But this time governments in rich countries have preserved households' incomes. Handouts through wage subsidies, furlough schemes and expanded welfare benefits amount to 5% of GDP. In the second quarter of the year households' disposable incomes in the G7 group of large economies were about $100bn higher than they were before the pandemic, even as jobs disappeared by the millions.

第二大因素是财政政策。财政政策在解释房价上涨上可能更为重要。在正常的经济衰退之下,当人们失去工作、收入下降时,丧失抵押品赎回权会拖低房价——这不仅会增加市场上的房屋供应,还会让前房主的信用记录上留下污点,使他们更难再次贷款。不过这次,发达国家的政府保护了家庭收入,通过工资补贴、休假计划和扩大福利发放的补贴达到了GDP的5%。今年第二季度,尽管有数百万人失去了工作,由大型经济体组成的七国集团(G7)的家庭可支配收入依然比疫情爆发前高出了约1000亿美元,

Other measures directly support the housing market. Spain, for instance, has allowed borrowers to suspend their mortgage repayments. Japan's regulators have asked banks to defer principal repayments on mortgages, and the Netherlands temporarily banned foreclosures. In the second quarter the number of owner-occupied mortgaged properties that were repossessed in Britain was 93% lower than in the same period in 2019, the result of policies that dissuade repossessions. In America foreclosures, as a share of all mortgages, are at their lowest level since 1984.

还有其它一些直接支持房地产市场的措施。例如,西班牙已经允许借款人暂停还贷。日本的监管机构已要求银行推迟偿还抵押贷款的本金。英国第二季度被收回的业主自住抵押房产的数量同比减少了93%,这是劝阻收回房产政策的结果。在美国,丧失抵押品赎回权占所有抵押贷款的比例处于1984年以来的最低水平。

QQ截图20201029161928.png

The third factor behind the unlikely global housing boom relates to changing consumer preferences. In 2019 households in the median OECD country devoted 19% of spending to housing costs. With a fifth of office workers continuing to work from home, many potential buyers may want to spend more on a nicer place to live. Already there is evidence that people are upgrading their household appliances.

全球房地产意外出现的繁荣背后的第三个因素与消费者偏好的变化有关。2019年,经合组织中位数国家的家庭将19%的支出用于住房成本。随着五分之一的上班族继续在家工作,许多潜在的买家可能想要花更多的钱在更好的地方居住。已有证据表明,人们正在升级家用电器。

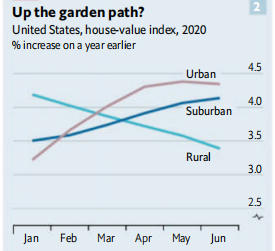

People also seem to be looking for more space—which, all else being equal, raises house prices. Though the New York and San Francisco housing markets look weak, there is little wider evidence to support the idea that people are fleeing cities for the suburbs, at least in America. Data from Zillow, a housing marketplace, suggest urban and suburban property prices are rising at roughly the same pace; price growth in the truly get-away-from-it-all areas is actually slowing. It seems more likely that people are looking for bigger houses near where they already live. In Britain prices of detached houses are rising at an annual rate of 4%, compared with 0.9% for flats, and the market for homes with gardens is livelier than for those without.

人们似乎也在寻找更多的空间,在其他条件相同的情况下,这就抬高了房价。尽管纽约和旧金山的房地产市场看起来很疲软,但至少在美国,没有更广泛的证据支持人们正从城市迁往郊区这一观点。房地产市场Zillow的数据显示,城市和郊区房价的上涨速度大致相同;在那些真正可以摆脱危机的地区,价格增长实际上正在放缓。人们似乎更有可能在他们已经居住的地方附近寻找更大的房子。在英国,独立住宅的价格正以每年4%的速度上涨,而公寓仅为0.9%,此外,带花园的住宅市场比不带花园的住宅市场更为活跃。

Can house prices continue their upward march? Governments are slowly winding down their economic-rescue plans, and no one knows what will happen once support ends. But lower demand for housing may run up against lower supply. High levels of economic uncertainty deter investment: in America housebuilding has fallen by 17% since covid-19 struck. The experience of the last recession suggests that even when the economy recovers, construction lags behind. It may take more than the deepest downturn since the Depression to shake the housing market's foundations.

房价还会持续上涨吗?各国政府正逐渐缩减经济救助计划,没有人知道一旦救助结束会发生什么,但住房需求的减少可能会与供给的减少相冲突。经济的极具不稳定性将推迟投资:美国自新冠爆发以来住房建造已经减少了17%。上一次经济衰退的经验表明,经济即使复苏了,建筑行业仍然滞后。要想动摇房地产市场的根基,经济衰退还得再加把劲儿!

来源:可可英语

参与评论